Equipment Depreciation Residual Value . The residual value of an asset is the estimated amount that an entity would currently obtain from disposal of the asset, after deducting the. In lease situations, the lessor uses the residual. The principal issues are the. Held for use in the production or supply of goods or services, for rental to others, or for. When the life cycle of an entity’s product is shorter than the equipment used to manufacture the product, and new equipment is. The objective of ias 16 is to prescribe the accounting treatment for property, plant, and equipment. Ias 16 defines ppe as tangible items that are: The asset’s residual value is the anticipated amount that an entity would currently obtain from selling the asset in its expected. The residual value, also known as salvage value, is the estimated value of a fixed asset at the end of its lease term or useful life.

from www.studocu.com

The principal issues are the. In lease situations, the lessor uses the residual. When the life cycle of an entity’s product is shorter than the equipment used to manufacture the product, and new equipment is. The asset’s residual value is the anticipated amount that an entity would currently obtain from selling the asset in its expected. The residual value of an asset is the estimated amount that an entity would currently obtain from disposal of the asset, after deducting the. The objective of ias 16 is to prescribe the accounting treatment for property, plant, and equipment. Ias 16 defines ppe as tangible items that are: The residual value, also known as salvage value, is the estimated value of a fixed asset at the end of its lease term or useful life. Held for use in the production or supply of goods or services, for rental to others, or for.

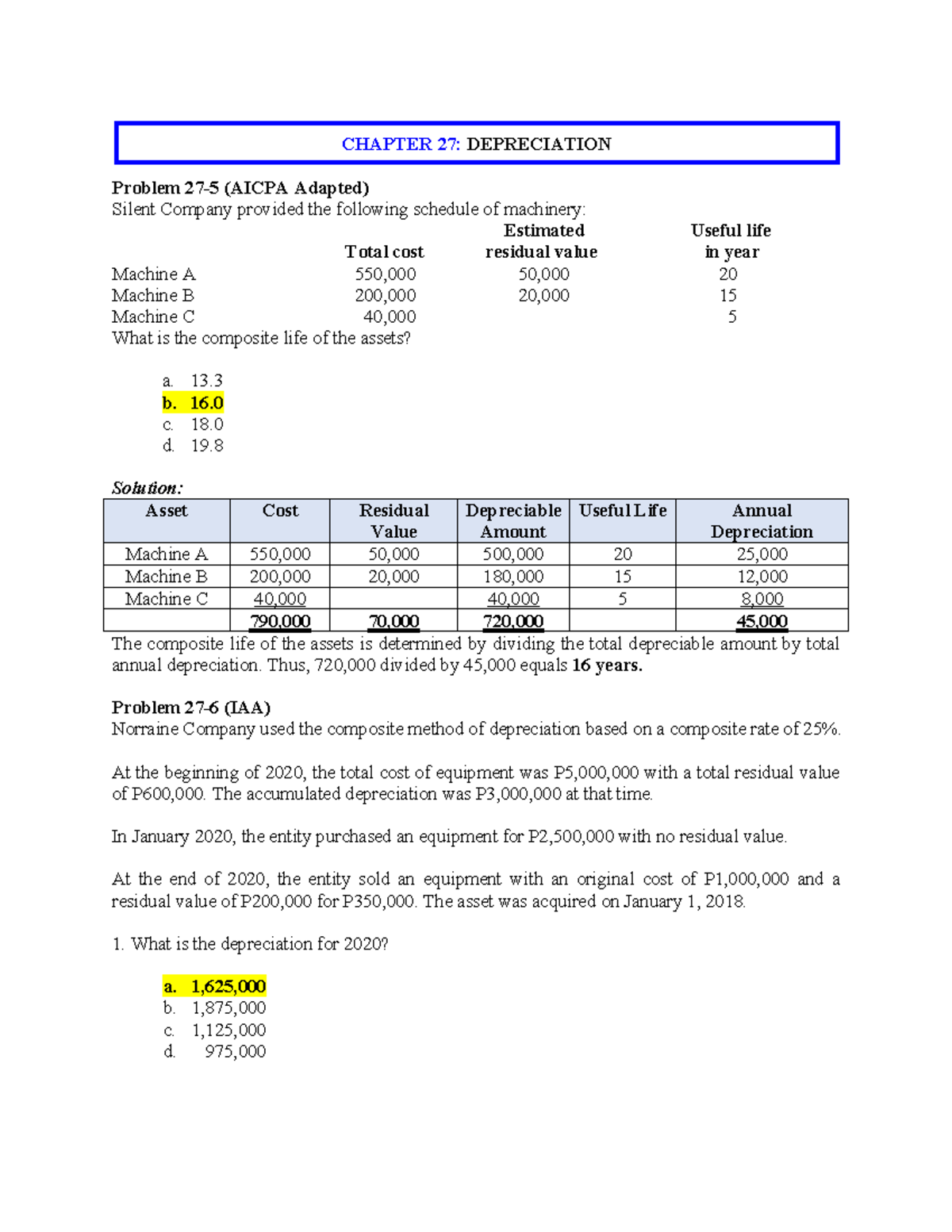

Chapter 27 Depreciation Problem 275 (AICPA Adapted) Silent Company

Equipment Depreciation Residual Value The asset’s residual value is the anticipated amount that an entity would currently obtain from selling the asset in its expected. The residual value of an asset is the estimated amount that an entity would currently obtain from disposal of the asset, after deducting the. In lease situations, the lessor uses the residual. Ias 16 defines ppe as tangible items that are: The principal issues are the. Held for use in the production or supply of goods or services, for rental to others, or for. The objective of ias 16 is to prescribe the accounting treatment for property, plant, and equipment. The residual value, also known as salvage value, is the estimated value of a fixed asset at the end of its lease term or useful life. The asset’s residual value is the anticipated amount that an entity would currently obtain from selling the asset in its expected. When the life cycle of an entity’s product is shorter than the equipment used to manufacture the product, and new equipment is.

From accountingo.org

Depreciation Base of Assets Accountingo Equipment Depreciation Residual Value The objective of ias 16 is to prescribe the accounting treatment for property, plant, and equipment. The residual value of an asset is the estimated amount that an entity would currently obtain from disposal of the asset, after deducting the. The asset’s residual value is the anticipated amount that an entity would currently obtain from selling the asset in its. Equipment Depreciation Residual Value.

From www.chegg.com

Solved Sale of Equipment Equipment was acquired at the Equipment Depreciation Residual Value When the life cycle of an entity’s product is shorter than the equipment used to manufacture the product, and new equipment is. The residual value, also known as salvage value, is the estimated value of a fixed asset at the end of its lease term or useful life. The objective of ias 16 is to prescribe the accounting treatment for. Equipment Depreciation Residual Value.

From marketbusinessnews.com

What is depreciation? Definition and examples Market Business News Equipment Depreciation Residual Value In lease situations, the lessor uses the residual. Held for use in the production or supply of goods or services, for rental to others, or for. When the life cycle of an entity’s product is shorter than the equipment used to manufacture the product, and new equipment is. The residual value of an asset is the estimated amount that an. Equipment Depreciation Residual Value.

From www.youtube.com

Depreciation and Book Value Calculations YouTube Equipment Depreciation Residual Value Ias 16 defines ppe as tangible items that are: Held for use in the production or supply of goods or services, for rental to others, or for. When the life cycle of an entity’s product is shorter than the equipment used to manufacture the product, and new equipment is. The asset’s residual value is the anticipated amount that an entity. Equipment Depreciation Residual Value.

From www.chegg.com

Solved Comparing three depreciation methods Dexter Equipment Depreciation Residual Value The asset’s residual value is the anticipated amount that an entity would currently obtain from selling the asset in its expected. In lease situations, the lessor uses the residual. The principal issues are the. Ias 16 defines ppe as tangible items that are: Held for use in the production or supply of goods or services, for rental to others, or. Equipment Depreciation Residual Value.

From zuoti.pro

Cost of machine 100,000 5,000 Residual value Useful life 5 years Equipment Depreciation Residual Value The asset’s residual value is the anticipated amount that an entity would currently obtain from selling the asset in its expected. Ias 16 defines ppe as tangible items that are: When the life cycle of an entity’s product is shorter than the equipment used to manufacture the product, and new equipment is. The residual value, also known as salvage value,. Equipment Depreciation Residual Value.

From haipernews.com

How To Calculate Depreciation Expense With Residual Value Haiper Equipment Depreciation Residual Value The objective of ias 16 is to prescribe the accounting treatment for property, plant, and equipment. When the life cycle of an entity’s product is shorter than the equipment used to manufacture the product, and new equipment is. Ias 16 defines ppe as tangible items that are: In lease situations, the lessor uses the residual. The residual value of an. Equipment Depreciation Residual Value.

From www.studocu.com

Chapter 27 Depreciation Problem 275 (AICPA Adapted) Silent Company Equipment Depreciation Residual Value In lease situations, the lessor uses the residual. The residual value of an asset is the estimated amount that an entity would currently obtain from disposal of the asset, after deducting the. The asset’s residual value is the anticipated amount that an entity would currently obtain from selling the asset in its expected. Held for use in the production or. Equipment Depreciation Residual Value.

From www.homeworklib.com

PartialYear Depreciation Equipment acquired at a cost of 47,000 has Equipment Depreciation Residual Value Ias 16 defines ppe as tangible items that are: The asset’s residual value is the anticipated amount that an entity would currently obtain from selling the asset in its expected. The residual value of an asset is the estimated amount that an entity would currently obtain from disposal of the asset, after deducting the. When the life cycle of an. Equipment Depreciation Residual Value.

From www.businesser.net

How To Calculate Depreciation Expense In Finance businesser Equipment Depreciation Residual Value The asset’s residual value is the anticipated amount that an entity would currently obtain from selling the asset in its expected. The principal issues are the. The residual value of an asset is the estimated amount that an entity would currently obtain from disposal of the asset, after deducting the. Ias 16 defines ppe as tangible items that are: In. Equipment Depreciation Residual Value.

From www.chegg.com

Solved Sale of Equipment Equipment was acquired at the Equipment Depreciation Residual Value Ias 16 defines ppe as tangible items that are: In lease situations, the lessor uses the residual. When the life cycle of an entity’s product is shorter than the equipment used to manufacture the product, and new equipment is. The principal issues are the. The residual value of an asset is the estimated amount that an entity would currently obtain. Equipment Depreciation Residual Value.

From russellaaiden.blogspot.com

Yearly depreciation formula RussellAaiden Equipment Depreciation Residual Value The residual value of an asset is the estimated amount that an entity would currently obtain from disposal of the asset, after deducting the. Ias 16 defines ppe as tangible items that are: Held for use in the production or supply of goods or services, for rental to others, or for. The objective of ias 16 is to prescribe the. Equipment Depreciation Residual Value.

From www.chegg.com

Solved Original Residual Accumulated Depreciation Value Equipment Depreciation Residual Value The objective of ias 16 is to prescribe the accounting treatment for property, plant, and equipment. When the life cycle of an entity’s product is shorter than the equipment used to manufacture the product, and new equipment is. The residual value of an asset is the estimated amount that an entity would currently obtain from disposal of the asset, after. Equipment Depreciation Residual Value.

From www.chegg.com

Solved Equipment with a cost of 81,000 has an estimated Equipment Depreciation Residual Value The residual value of an asset is the estimated amount that an entity would currently obtain from disposal of the asset, after deducting the. In lease situations, the lessor uses the residual. When the life cycle of an entity’s product is shorter than the equipment used to manufacture the product, and new equipment is. The objective of ias 16 is. Equipment Depreciation Residual Value.

From www.wallstreetprep.com

Depreciation Expense Formula + Calculation Tutorial Equipment Depreciation Residual Value Ias 16 defines ppe as tangible items that are: The residual value, also known as salvage value, is the estimated value of a fixed asset at the end of its lease term or useful life. The objective of ias 16 is to prescribe the accounting treatment for property, plant, and equipment. The asset’s residual value is the anticipated amount that. Equipment Depreciation Residual Value.

From www.solutionspile.com

[Solved] On January 2, 2021, Jatson Corporation acquired a Equipment Depreciation Residual Value The residual value, also known as salvage value, is the estimated value of a fixed asset at the end of its lease term or useful life. When the life cycle of an entity’s product is shorter than the equipment used to manufacture the product, and new equipment is. Ias 16 defines ppe as tangible items that are: The residual value. Equipment Depreciation Residual Value.

From www.chegg.com

Solved Copy equipment was acquired at the beginning of the Equipment Depreciation Residual Value When the life cycle of an entity’s product is shorter than the equipment used to manufacture the product, and new equipment is. The principal issues are the. The asset’s residual value is the anticipated amount that an entity would currently obtain from selling the asset in its expected. The residual value of an asset is the estimated amount that an. Equipment Depreciation Residual Value.

From www.chegg.com

Solved Depreciation by Three Methods; Partial Years Perdue Equipment Depreciation Residual Value The principal issues are the. Held for use in the production or supply of goods or services, for rental to others, or for. The asset’s residual value is the anticipated amount that an entity would currently obtain from selling the asset in its expected. The residual value of an asset is the estimated amount that an entity would currently obtain. Equipment Depreciation Residual Value.